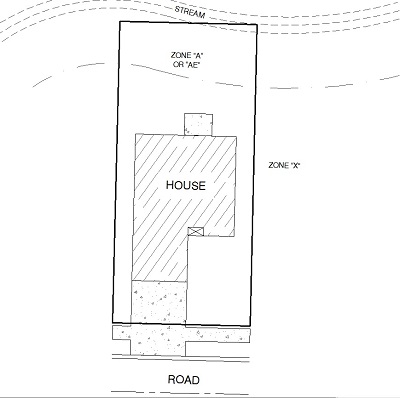

SITUATION 1

SITUATION 1

Part of the property is in Zone “A” or “AE”, house is in Zone “X”. Usually a simple elevation certificate can demonstrate that the house is in Zone “X” and the flood insurance requirement is waived. A Base Flood Elevation is not important. Some lenders may still require a LOMA just to “be on the safe side”, though this is largely unnecessary.

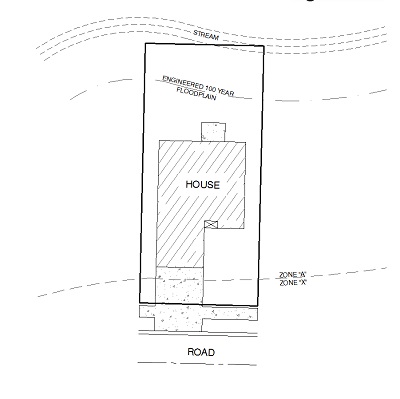

SITUATION 2

SITUATION 2

House in Zone “A” but outside actual flood plain. Here the home-owner is a victim of exaggerated flood zone lines and has two options, to pay flood insurance at high risk rate class or pursue a Letter of Map Amendment (LOMA).

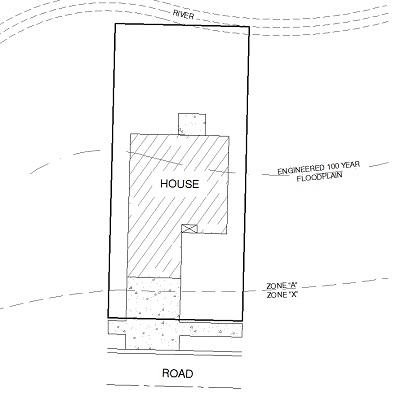

SITUATION 3

SITUATION 3

House in Zone “A” and inside the actual flood plain. Flood insurance will be required, the only thing to be determined is the premium amount. Although an Elevation Certificate will be required, the premium class will be highest risk without a valid BFE. An option is to obtain a private study to determine the BFE. Depending on the probable elevation relevance to the flood plain, the home-owner may save money by obtaining a private study.

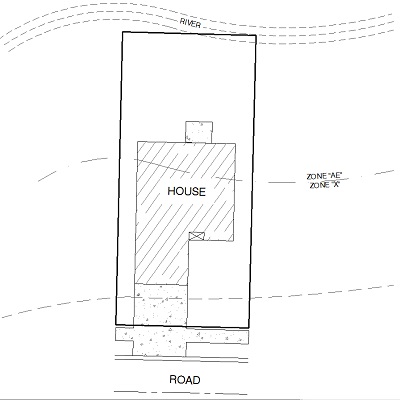

SITUATION 4

SITUATION 4

House in Zone “AE”. Flood insurance will be required, and the Elevation Certificate must relate the structure to the published BFE. Flood insurance rates will be partly based on the elevation of the structures relevant to the BFE.